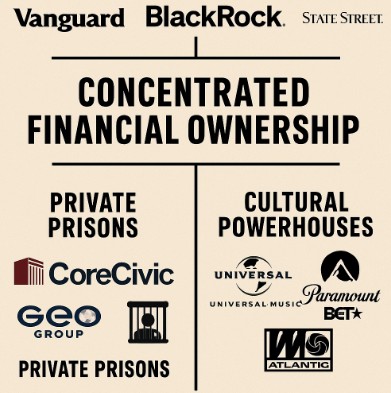

Finance, Media, and the Carceral System in One Portfolio

A small circle of financial giants—Vanguard, BlackRock, and State Street—holds outsized stakes in both private prison operators (CoreCivic and GEO Group) and cultural powerhouses (Paramount/BET, Universal Music Group, Warner/Atlantic). These asset managers do not run the day-to-day operations of these companies, but their concentrated ownership ensures they profit from—and can exert influence over—two industries that shape both confinement and culture.

This overlap raises pressing questions: What incentives guide shareholder decision-making when the same firms stand to benefit from incarceration and from cultural production? How does voting power at annual meetings reinforce or challenge practices that disproportionately harm Black communities? And does the structure of index capitalism itself entrench these harms by design?

Correcting a common misconception is also important: while Vanguard is often cited as the top shareholder in CoreCivic, the most recent data show that BlackRock is currently the largest institutional holder of both CoreCivic (CXW) and GEO Group (GEO), with Vanguard typically in the number two position. The problem, then, is not a single firm—it is the system of concentrated financial ownership that profits from both mass incarceration and the cultural narratives surrounding it.

Ownership facts as of mid-2025

- Private prisons:

- CoreCivic (CXW): Top holders include BlackRock (~16%) and Vanguard (~11–12%).

- GEO Group (GEO): Top holders include BlackRock (~15%) and Vanguard (~10–11%).

- Media & music stakes (illustrative):

- BET is within Paramount (now Paramount Skydance); the company decided not to sell BET and has recently reaffirmed it will keep the brand. Vanguard is among the largest institutional holders of Paramount stock.

- Universal Music Group (UMG): Significant shareholders include Vivendi, Tencent, Pershing Square, with Vanguard/BlackRock holding smaller (single-digit) percentages as index investors.

- Atlantic Records sits under Warner Music Group (WMG) (not “Time Warner” and not “Time Earner”). WMG is controlled by Access Industries; index funds (including Vanguard) hold minority positions via funds.

The Big Three—Vanguard, BlackRock, and State Street—regularly appear among the largest institutional holders of firms across sectors. In private corrections, CoreCivic and GEO Group feature the Big Three among their top shareholders. In media and music, Paramount (BET), Universal Music Group (UMG), and Warner Music Group (WMG/Atlantic) likewise report substantial index-fund stakes alongside controlling owners (e.g., Access Industries at WMG; large strategic holders and consortia at UMG). Exact ranks fluctuate, but the pattern is consistent: the same asset-management complexes sit behind both cultural distribution and carceral capacity.

This commonality does not mean index funds dictate editorial decisions or prison operations. It does mean their stewardship teams (through proxy voting and engagement) influence board composition, executive incentives, and the boundaries of what strategies are considered “normal” or “shareholder-value enhancing.

Bottom line: The same Big Three index complexes (Vanguard, BlackRock, State Street) appear again and again as top holders across these sectors—even when they’re not the #1 holder in every single firm.

Why “common ownership” matters—even if funds are “passive”

Scholars call this phenomenon common ownership: when a small set of investors simultaneously owns significant stakes in multiple “competing” or cross-sector firms. Evidence (and debate) suggests it can dampen competition and shape firm behavior through proxy voting, engagement, and executive incentives.

- Azar, Schmalz & Tecu (2018) show common ownership correlated with higher airline ticket prices on routes where the Big Three held overlapping stakes. While the airline context differs from media or prisons, the mechanism—shared investors across putative competitors—generalizes.

- Bebchuk & Hirst (2019) argue index fund stewardship choices materially affect corporate governance across the economy due to their scale and perpetuity.

What this implies here:

When the same index complexes profit from incarceration capacity and own major stakes in cultural distributors, they may (even unintentionally) normalize incentives that prioritize stable cash flows and risk-averse narratives—over reforms that would reduce incarceration or materially challenge profitable status quos.

The justice dimension: Who pays the human cost?

The United States continues to incarcerate nearly two million people, with Black communities bearing a disproportionate share of that burden. Despite decades of reform debates, racial disparities remain stark: Black Americans are imprisoned at far higher rates than their white counterparts.

Private prison corporations such as CoreCivic and GEO Group are still deeply embedded in the machinery of incarceration. In particular, they play a pivotal role in the growth of immigration detention and remain central to federal and state plans to expand detention capacity—even as watchdogs and journalists continue to document troubling patterns of neglect, abuse, and inadequate oversight.

This creates a profound ethical tension. When large asset managers profit simultaneously from cultural industries—through advertising revenue and music streaming—and from high occupancy rates in detention centers and prisons, their portfolios are structured around both the production of culture and the perpetuation of carceral systems. The implicit incentive is not transformation but stability: sustaining practices that disproportionately harm Black communities, even if no single investor explicitly directs such outcomes.

A biblical-worldview lens: justice, dignity, stewardship

From a Christian ethical standpoint, justice is never limited to retribution. True justice is restorative—it seeks shalom, the wholeness of community, and honors the God-given dignity of every person. Stewardship, likewise, calls us to direct resources toward the flourishing of the vulnerable rather than the exploitation of their vulnerability.

When applied to questions of corporate and investor ownership, these convictions take on concrete form:

- Justice: Investment strategies should not be built on systems that reliably generate profit through harm—especially when those harms fall disproportionately on Black communities.

- Dignity: Shareholders and corporate leaders should use their influence to uphold humane standards—ensuring access to healthcare, preserving family connections, and protecting due process—while dismantling financial incentives that depend on keeping people behind bars.

- Stewardship: Proxy votes, shareholder engagement, and public policy advocacy should be guided by a commitment to reduce incarceration where consistent with public safety, and to expand alternatives rooted in treatment, re-entry support, and stable housing.

This framework challenges Christians to see capital not as neutral, but as a moral force that must be oriented toward mercy, justice, and the common good.

What this concentration of ownership “says” about our systems?

Financial power is not just influence—it is infrastructure. The same vast pools of capital sit quietly behind television networks, record labels, streaming platforms, and private prison operators. This overlap is not evidence of a hidden conspiracy; it is the logic of index capitalism at scale. Yet by concentrating ownership across sectors, these funds create portfolio-wide incentives that can directly conflict with the pursuit of justice.

Accountability, in this system, is diffused upward. No single studio executive or prison warden singlehandedly sustains mass incarceration. But stewardship teams at asset managers vote on board members, executive pay, and long-term strategy. In doing so, they help determine what counts as acceptable practice and what risks corporations are permitted to ignore.

The result is a troubling convergence: cultural production and carceral policy can become mutually reinforcing. Media narratives shape public imagination about crime and punishment, while prison companies profit when punitive approaches prevail. When the same investors benefit from both, the cycle of incarceration and its disproportionate impact on Black communities risks becoming entrenched not by explicit design, but by the structural incentives of shared ownership.

Policy Pathways for Accountability and Reform

End profit-driven prison contracts.

Private prison deals often guarantee a minimum number of filled beds. This means taxpayers keep paying whether facilities are full or not—creating a perverse incentive to keep them occupied. Contracts should instead reward outcomes like safety, health, and successful re-entry.

Shine a light on conditions.

Transparency saves lives. Public dashboards tracking deaths in custody, medical care, staffing, grievances, and solitary confinement would hold facilities accountable and give communities the data they need to demand change.

Fund proven alternatives.

Every dollar locked into incarceration is a dollar not spent on solutions that work. Housing-first re-entry programs, addiction treatment, restorative justice, and community-based supervision consistently lower recidivism rates. The evidence is clear: investment in people is safer and cheaper than investment in cells.

Hold investors to higher standards.

Universities, churches, retirement funds, and everyday investors have power. They can file shareholder proposals demanding stronger healthcare standards and the end of occupancy guarantees. And when boards ignore human rights, investors should vote against directors and executive pay packages. Money talks—so let it speak for justice.

Shift the story.

The same big funds own stakes in both prisons and media. That means they profit from incarceration and from culture. Media firms should commit resources to evidence-based storytelling that lifts up reform, re-entry success, and harm-reduction—not just narratives that normalize punishment.

Treat incarceration as systemic risk.

Just like climate change or the opioid crisis, mass incarceration destabilizes communities and economies. Asset managers and institutions should publish stewardship policies that name incarceration as a systemic risk requiring portfolio-wide action.

Civil Discernment: Reading Between the Lines of Ownership

At first glance, index funds appear neutral—simply a passive vehicle tracking markets. But concentrated ownership by firms like Vanguard, BlackRock, and State Street demands a deeper look. These asset managers are not small investors; they are the largest shareholders in both private prison operators (CoreCivic, GEO Group) and the cultural industries that shape narratives and identity (BET, Universal Music Group, Warner/Atlantic).

While they do not set the day-to-day agendas of these corporations, their financial power is anything but passive. They profit when prisons expand and profit when music sells, even as those two systems intersect in ways that disproportionately harm Black communities. The same Black communities targeted by over-incarceration are also cultural producers whose art and narratives are monetized under the same shareholder umbrellas.

This convergence raises moral and structural questions:

- Incentives: Does capital accumulation depend on reinforcing cycles of harm?

- Voting Power: When shareholder votes determine corporate policy, how much influence do these firms have over whether private prisons expand contracts—or whether media corporations amplify or suppress particular voices?

- Entrenchment of Inequities: If the same financial institutions are positioned to benefit from both incarceration and entertainment, are systemic inequities built directly into the flows of capital itself?

Correcting the record also matters: while Vanguard is often cited as the primary owner of CoreCivic, recent data show that BlackRock holds the top spot in both CoreCivic and GEO Group, with Vanguard close behind. This distinction underscores that no single firm monopolizes the problem—rather, it is the structure of index capitalism itself that links profit motives across prisons and cultural institutions.

Discernment requires asking whether we accept a financial ecosystem that treats mass incarceration and cultural production as just two profitable industries among many. If so, we risk normalizing a cycle in which the harms experienced by marginalized communities become permanently capitalized, with little incentive to disrupt them.

Zooming Out: What This Means in the Larger Context

Step back far enough and this story stops being a list of shareholders and starts to look like infrastructure. When the same capital pools sit behind the companies that shape our stories and the companies that profit from confinement, the gravitational pull of the portfolio can nudge decisions toward what is predictable and safe for cash flows—even if that predictability rests on punitive systems that destabilize families and neighborhoods. No memo needs to be sent; incentives travel silently through boardrooms, proxy votes, and pay plans (Bebchuk & Hirst, 2019).

In democratic life, narrative power matters as much as formal power. Media and music do more than entertain; they establish which problems feel urgent and which solutions sound plausible. If universal investors are simultaneously exposed to advertising revenue, streaming growth, and the steady rents of incarceration and detention, portfolio-wide risk management can favor incrementalism over accountability narratives. The research on common ownership shows how overlapping investors can alter competitive conduct in subtle, non‑conspiratorial ways (Azar, Schmalz, & Tecu, 2018). Translate that to culture and punishment, and the public square risks becoming more comfortable with the world as it already is.

There is also a hard‑headed fiduciary angle: index funds are universal owners. They hold the whole market—and when mass incarceration extracts human capital, increases public costs, and worsens health, those harms boomerang back into the broader economy the very same funds own. These are portfolio externalities, not easily diversified away. The numbers remain stark: nearly two million people behind bars, with persistent racial disparities and heavy reliance on immigration detention (Prison Policy Initiative, 2025; The Sentencing Project, 2024, 2025).

Policy design either amplifies or mutes those incentives. Guaranteed bed‑occupancy clauses and per‑diem payment structures reward filled cells rather than safe facilities or successful re‑entry. Tying compensation to outcomes—lower recidivism, timely medical care, family contact, staff safety—pulls in the opposite direction. Oversight hearings and reporting on detention expansion show how contract design and procurement choices cascade into everyday conditions (U.S. Senate Judiciary Committee, 2025; Washington Post, 2025).

For faith‑rooted readers, the theological stakes are clear. If every person bears the image of God, stewardship cannot monetize precarity. Justice aims at shalom—repair, not mere retribution. That ethic belongs in proxy voting guidelines as much as it belongs in Sunday sermons: oppose occupancy guarantees, demand human‑rights due diligence, escalate votes against directors where abuse persists, and insist on real transparency about deaths in custody and access to care.

The metrics that matter should change accordingly. Instead of celebrating occupancy rates or EBITDA, measure recidivism reduction, hours of family contact enabled, the speed of medical response, grievances resolved, assaults prevented, and successful transitions to stable housing and work. In media, commit resources to evidence‑based justice storytelling, so audiences understand what actually reduces harm.

And at the personal level, ordinary investors are not powerless. Review the holdings in your 401(k) or IRA. Ask your fund provider for its human‑rights stewardship policy and how it votes on detention and prison risks. Support community groups that make decarceration possible— re‑entry housing, record‑sealing clinics, restorative‑justice programs. Share and fund creators who tell the fuller truth about safety and repair.

The larger context, then, is not about catching a villain. It is about redesigning incentives—from contracts to capital—so portfolios grow by healing communities rather than by holding them.

The Strategy Problem: Profiting on Both Ends

From a portfolio perspective, mass incarceration and mass culture are not separate stories—they are two sides of the same balance sheet. Index funds and asset managers hold stakes in both the companies that produce cultural content and those that profit from incarceration. This creates what looks, in financial terms, like a “hedge”:

- If incarceration expands, private prison companies benefit through occupancy guarantees, per-diem payments, and contracts tied to immigration detention growth.

- If incarceration sparks public debate, media and music corporations monetize that narrative—through news coverage, storytelling, or cultural output that shapes public perception.

In other words, the same investors can win whether punitive systems expand or the cultural industries tell stories about them. Cash flows are stabilized across both sides of the equation.

This is not about a secret conspiracy; it is about strategic structure. The design of index capitalism creates portfolio-wide incentives to prefer stability over disruption. Reform—whether decarceration or radical shifts in cultural narratives—introduces uncertainty. Stability, by contrast, protects predictable returns.

That is why this issue is more than moral or political—it is strategic. The financial system, by profiting on both confinement and culture, embeds a bias toward preserving the status quo, even when that status quo extracts disproportionate costs from Black communities.

Call to Action: From Awareness to Accountability

Awareness is only the first step. The deeper challenge is deciding what to do with the knowledge that major asset managers profit from both incarceration and culture.

- Rethink Investment Choices

Many retirement accounts, 401(k)s, and index funds automatically channel money into these firms. Explore socially responsible or faith-based funds that screen out private prisons and companies with harmful track records. Ask your employer or financial advisor about ethical options. - Leverage Shareholder Power

Even small investors can make their voices heard through proxy voting. Shareholders can pressure asset managers to support resolutions on prison divestment, corporate accountability, and equitable cultural representation. - Support Policy Reform

Push for legislation requiring greater transparency in corporate ownership structures and for regulations that limit the privatization of prisons. Public pressure has already pushed some banks to stop financing prison companies—policy can go further. - Amplify Community Voices

Center and support the leadership of Black communities most impacted by these overlapping systems. Whether through supporting grassroots organizations, local artists, or community-led justice reform, redirecting resources helps break the cycle of harm. - Practice Civic Discernment

Share these connections with others. Ask your church group, book club, or classroom: What does it mean for our communities when the same shareholders profit from mass incarceration and mass culture? Reflection leads to accountability, and accountability can shift systems.

The link between private prisons and cultural industries is not accidental—it is structural. Discernment reminds us that these systems are designed to benefit from both human confinement and human creativity. Action requires refusing to accept that design as inevitable.

We Want to Hear From You

This conversation isn’t just about numbers on a balance sheet—it’s about the lives, communities, and futures shaped by where capital flows. Your voice matters in shaping what justice, dignity, and stewardship look like in practice.

- Do you think investors should have a responsibility to challenge prison contracts and harmful business models?

- How should media companies tell stories about incarceration and justice?

- What role can communities of faith, civic groups, or everyday investors play in reshaping these incentives?

- What questions does this raise for your own financial, civic, or ethical choices?

💬 Share your thoughts in the comments or join the conversation on social media with the hashtag #CenterlineJustice.

Together, discernment can turn into action.

References

Azar, J., Schmalz, M. C., & Tecu, I. (2018). Anticompetitive effects of common ownership. The Journal of Finance, 73(4), 1513–1565.

Bebchuk, L. A., & Hirst, S. (2019). Index funds and the future of corporate governance: Theory, evidence, and policy. Columbia Law Review, 119(8), 2029–2145.

CoreCivic, Inc. (CXW) — Institutional holders (2025). Nasdaq.com.

CoreCivic, Inc. (CXW) — Ownership snapshot (2025). Investing.com.

GEO Group, Inc. (GEO) — Institutional holders (2025). Yahoo Finance.

GEO Group, Inc. (GEO) — Ownership snapshot (2025). Fintel.

Paramount (BET parent) — Strategy and BET retention (Aug. 14, 2025). Reuters.

Paramount/BET — Not for sale (Aug. 13–14, 2025). TheWrap; Black Enterprise.

Paramount Global — Institutional holders (PARA) (2025). MarketBeat; Fintel.

Universal Music Group — Ownership snapshot (2025). Investing.com; Yahoo Finance; Morningstar.

Atlantic/WMG — Corporate structure updates (2024–2025). Warner Music Group newsroom.

Prison Policy Initiative. (2025, March 11). Mass incarceration: The whole pie 2025.

Prison Policy Initiative. (2024, April 1). Updated charts show the magnitude of prison and jail incarceration & racial disparities.

The Sentencing Project. (2024, May 21). Mass incarceration trends.

The Sentencing Project. (2025, August 12). Black disparities in youth incarceration.

American Oversight. (2025, May 8). Abusive conditions and private-industry ties to mass immigration detention.

Washington Post. (2025, Sept. 7). ICE plans to reopen troubled detention centers.

U.S. Senate Judiciary Committee (Durbin). (2025, May 1). Oversight of immigration detention expansion.

Institute for Faith & Learning (Baylor). (2011/2024 reprint). Divine justice as restorative justice (study guide).

Fischer, K. J. (2020). Biblical principles of government and criminal justice. Journal of Statesmanship & Public Policy.

Leary, S. (2017). A biblical critique of the U.S. prison system. Journal of Christian Legal Thought, 7(2).